Running a business, whether large or small, involves navigating various risks that could impact its financial health. From natural disasters to legal claims, the range of potential disruptions is vast. Business insurance is a fundamental tool that provides protection against such unforeseen events. It helps business owners minimize the financial damage from accidents, lawsuits, employee injuries, or interruptions. Without the right coverage, a single lawsuit or disaster could lead to substantial financial losses—or worse, business closure.

This guide is designed to provide a comprehensive understanding of business insurance. We’ll explore its types, why it’s essential, how to choose the right policy, cost factors, and how to manage risk effectively. Whether you’re a startup, a well-established business, or an entrepreneur looking to expand, this article will offer valuable insights into how to protect your business.

Chapter 1: Understanding Business Insurance

1.1 What is Business Insurance?

Business insurance is a broad category that encompasses several types of coverage designed to protect businesses from financial losses due to unexpected events. These events can range from property damage, theft, and employee injuries to legal liabilities and interruptions in business operations. Essentially, business insurance transfers risk from the business owner to an insurance company, which pays for the covered losses in exchange for premium payments.

Every business, regardless of its size or industry, is exposed to risks. A sole proprietor may face the same types of risks as a large corporation, though on a smaller scale. Without insurance, a small fire in a retail shop or a slip-and-fall accident in an office could lead to financial ruin. Business insurance serves as a safety net that ensures your company remains operational after such incidents.

1.2 The Role of Risk Management

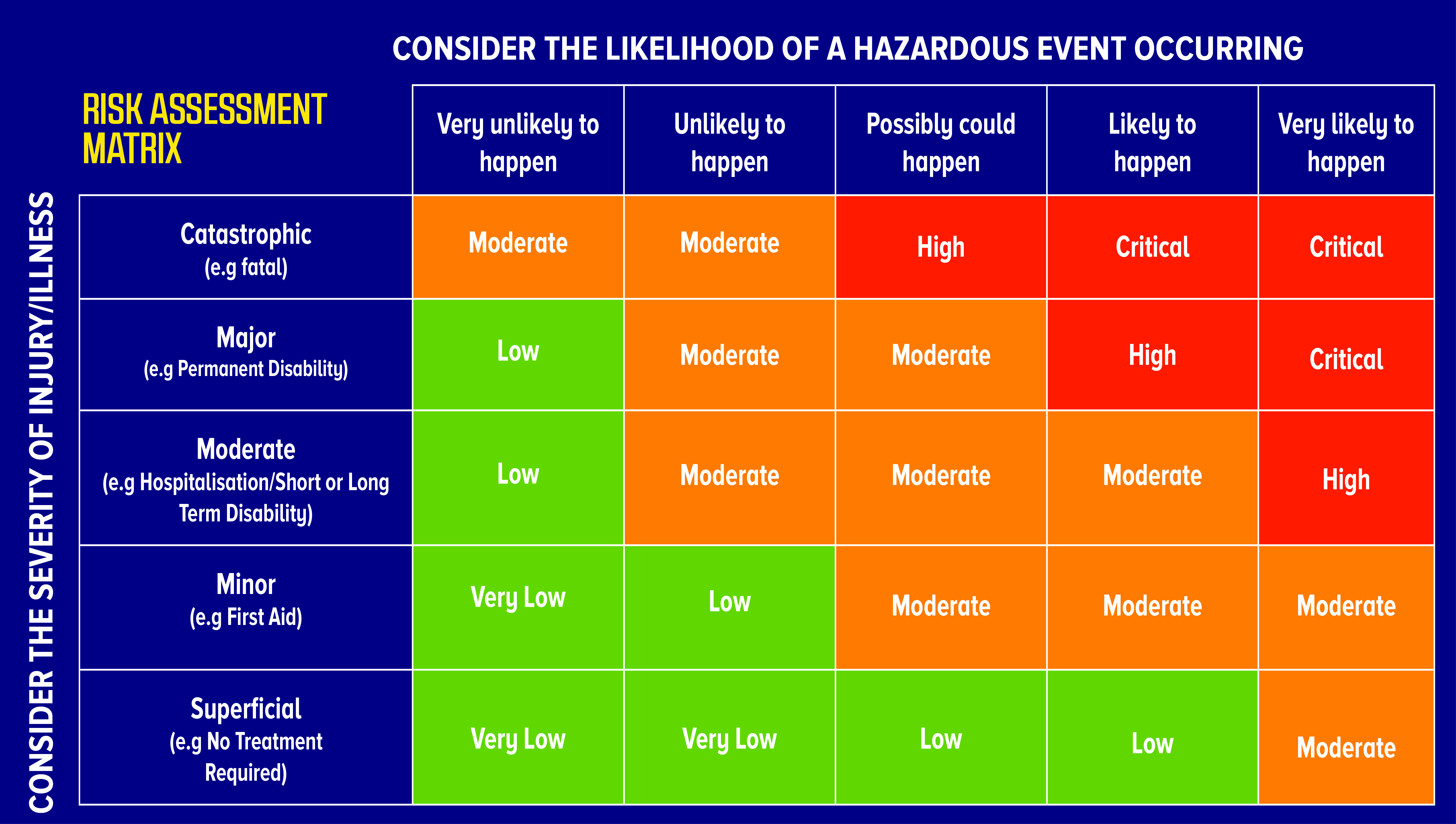

Before diving into the specifics of different insurance types, it’s important to understand risk management. Insurance is only one part of a broader risk management strategy. Risk management involves identifying potential risks, assessing their potential impact, and taking steps to mitigate them.

While insurance helps manage the financial consequences of a risk, preventive measures—such as implementing safety procedures, securing your premises, or installing fire alarms—reduce the likelihood of needing to file a claim in the first place. By reducing risks, businesses can lower their insurance premiums and avoid operational disruptions.

Chapter 2: Types of Business Insurance and Their Importance

Understanding the various types of business insurance available is key to selecting the right coverage for your company. Different types of insurance cover different risks, and businesses often need a combination of several policies to achieve comprehensive protection.

2.1 General Liability Insurance

General liability insurance is the cornerstone of most business insurance policies. It covers claims of bodily injury or property damage that result from your business operations. For instance, if a customer trips and falls in your store, general liability insurance covers medical costs and potential legal fees.

This type of insurance also protects against personal and advertising injury claims, such as if you accidentally infringe on another company’s trademark in an advertisement. General liability is important for businesses that interact with the public or operate in physical spaces where accidents can happen.

Examples of Covered Incidents:

- A client slips on a wet floor in your office and sues for medical expenses.

- A contractor damages a customer’s property while working on-site.

2.2 Property Insurance

Property insurance protects the physical assets of your business, including buildings, equipment, inventory, and furniture. If your business experiences damage due to fire, theft, vandalism, or certain natural disasters, property insurance will cover the cost to repair or replace damaged property.

There are two types of property insurance policies:

- Named-peril policy: This covers only the risks explicitly listed in the policy (e.g., fire, theft).

- All-risk policy: This provides broader coverage for any event, except those specifically excluded.

For businesses with a physical storefront, warehouse, or office space, property insurance is indispensable. Even home-based businesses need property insurance to cover business-related assets.

2.3 Workers’ Compensation Insurance

If your business employs workers, workers’ compensation insurance is mandatory in most states and countries. This coverage pays for medical care and lost wages if an employee is injured or falls ill due to a work-related incident. It also helps protect your business from employee lawsuits related to workplace injuries.

Even in office environments, workers can suffer injuries, such as carpal tunnel syndrome or slip-and-fall accidents. Workers’ compensation insurance ensures that employees are taken care of, and it minimizes the risk of litigation.

2.4 Professional Liability Insurance (Errors & Omissions)

Professional liability insurance, also known as errors and omissions (E&O) insurance, is crucial for businesses that provide specialized services or professional advice. It protects your business from claims related to negligence, errors, or omissions in the services you provide.

For example, if an architect makes an error in a building design that leads to costly repairs, the client may sue for damages. E&O insurance covers the legal costs and any settlement or judgment, protecting your financial stability.

This type of insurance is vital for industries such as consulting, real estate, law, finance, and healthcare, where the consequences of errors can be severe.

2.5 Product Liability Insurance

For businesses that manufacture, distribute, or sell products, product liability insurance is essential. It protects against claims arising from injuries or damages caused by defective products. If a product malfunctions and harms a customer, product liability insurance covers the legal costs associated with defending your business.

Lawsuits related to defective products can be expensive and time-consuming, especially if multiple customers are affected. Without product liability insurance, these costs could bankrupt a small business.

2.6 Business Interruption Insurance

Business interruption insurance, also known as business income insurance, covers the loss of income that a business suffers after a disaster that temporarily halts operations. This type of insurance is particularly important for businesses located in areas prone to natural disasters, such as hurricanes, floods, or earthquakes.

Business interruption insurance covers:

- Lost revenue due to temporary closure

- Fixed costs like rent and utilities

- Relocation expenses if your business needs to operate from a temporary location

Without this coverage, many businesses struggle to recover after a major disruption.

2.7 Cyber Liability Insurance

In today’s digital age, cyber threats pose a significant risk to businesses of all sizes. Cyber liability insurance protects your business from the financial consequences of data breaches, hacking incidents, and other cyberattacks. It covers legal fees, costs of notifying affected customers, and expenses related to restoring compromised data.

For businesses that store sensitive customer information or rely heavily on digital systems, cyber liability insurance is an absolute necessity.

Chapter 3: Why Businesses Need Insurance: Key Benefits and Protections

3.1 Legal Requirements and Compliance

In many regions, certain types of business insurance are legally required. For example, workers’ compensation insurance is mandatory in most jurisdictions if you have employees. Similarly, some states or countries may require businesses to carry general liability or professional liability insurance, especially for high-risk industries.

Failing to meet these legal obligations can result in significant penalties, fines, or even the forced closure of your business. It is critical to understand the specific insurance requirements in your area and industry to remain compliant.

3.2 Protecting Against Lawsuits and Liability

Lawsuits are an ever-present threat to any business, and even if your company operates ethically and responsibly, you can still be sued. Whether the lawsuit is related to a slip-and-fall injury, breach of contract, or a product defect, legal claims can be incredibly costly.

Business insurance protects your company from financial ruin by covering legal fees, court costs, settlements, and judgments. General liability insurance, professional liability insurance, and product liability insurance all play a role in protecting your business from different types of claims.

Examples of Legal Claims:

- A restaurant faces a lawsuit after a customer falls ill from contaminated food.

- A consultant is sued for providing faulty advice that results in a client’s financial loss.

3.3 Employee Protection

Your employees are one of your business’s most valuable assets. Ensuring their safety and well-being not only fosters loyalty but is often legally required. Workers’ compensation insurance ensures that employees who are injured on the job are compensated for medical expenses and lost wages.

In addition to workers’ compensation, businesses can offer health, disability, and life insurance to employees as part of a comprehensive benefits package. This fosters a positive work environment and makes the business more attractive to potential hires.

3.4 Protecting Physical Assets and Business Property

Physical assets such as buildings, equipment, and inventory represent a significant investment for many businesses. Property insurance ensures that your investment is protected in case of damage caused by fire, theft, vandalism, or certain natural disasters.

Whether you operate a retail store, manufacturing plant, or office space, property insurance is critical to maintaining business operations after an unforeseen event.

3.5 Ensuring Business Continuity During Disasters

Natural disasters, fires, and other disruptive events can cause your business to shut down temporarily. During this time, fixed expenses like rent, utilities, and payroll still need to be paid, even though your revenue may have halted. Business interruption insurance fills this gap by covering the lost income and ongoing costs.

For example, a restaurant that closes for two months after a fire could receive compensation for the lost profits during that period, allowing the owner to continue paying employees and suppliers. Without business interruption insurance, temporary shutdowns can lead to permanent closures.

Chapter 4: How to Choose the Right Business Insurance Policy

4.1 Assessing Business Risks

Every business has unique risks, and identifying them is the first step in choosing the right insurance. Some businesses face high risks of property damage (e.g., construction companies), while others may have greater liability risks (e.g., consulting firms or law offices).

Begin by analyzing your business’s operations, identifying potential threats, and understanding the likelihood of each risk materializing. For example, if you run a bakery, your main risks may include fire, food contamination, and equipment breakdown. A construction company, on the other hand, may need coverage for on-site accidents, equipment damage, and professional errors in project management.

4.2 Determining Mandatory vs. Optional Insurance

Some types of insurance are mandatory, while others are optional but highly recommended. As mentioned earlier, workers’ compensation insurance is required in most places for businesses with employees. Similarly, certain industries may have specific insurance requirements, such as professional liability insurance for healthcare providers or contractors.

Once you understand the mandatory coverages for your business, evaluate optional policies based on the risks identified in the previous section. While it might be tempting to skimp on coverage to save money, underinsuring your business could result in disastrous financial consequences.

4.3 Customizing Your Insurance Package

One of the advantages of business insurance is the ability to customize policies based on your specific needs. Insurance companies often offer package deals that combine different types of coverage into a single business owner’s policy (BOP), which typically includes general liability, property insurance, and business interruption insurance.

However, your business may have unique risks that require additional coverage beyond a standard package. For example, a tech company handling sensitive data may need cyber liability insurance, while a manufacturer may need product liability insurance.

When customizing your insurance package, consider:

- Business size and revenue: Larger businesses may require more extensive coverage.

- Industry: Different industries have unique risks that affect the types of coverage needed.

- Growth potential: As your business grows, your coverage needs may expand.

4.4 Reviewing and Adjusting Your Coverage Regularly

Business insurance isn’t a set-it-and-forget-it product. As your business evolves, so do its risks. For instance, if you expand into new locations, add employees, or offer new services, your insurance coverage may need to be updated.

Regularly review your policies—at least once a year or whenever major changes occur in your business operations. Consulting with an insurance broker or agent during these reviews can ensure that your coverage stays relevant and adequate.